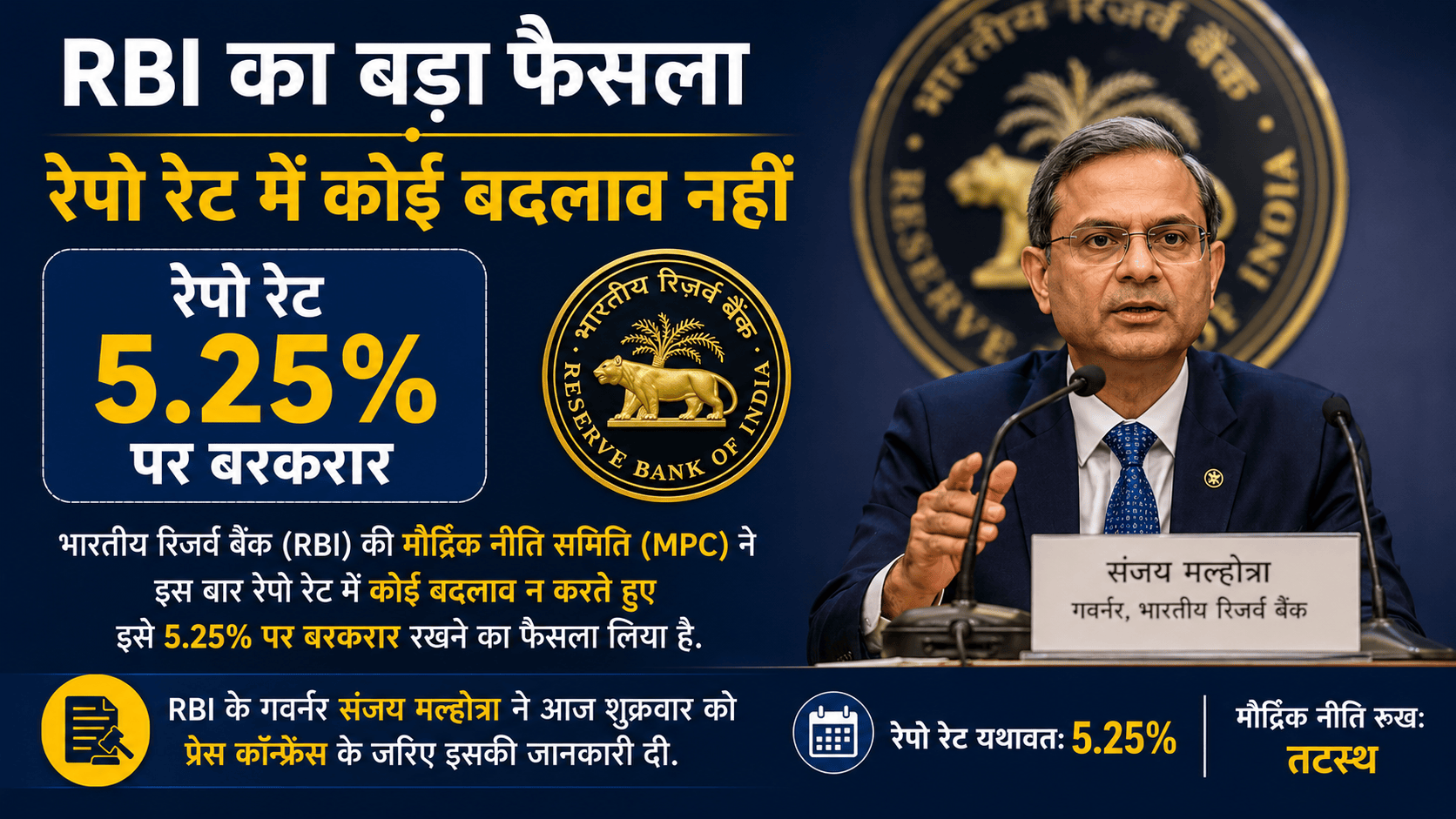

Introduction

EMI The Reserve Bank of India (RBI) recently announced a cut in the repo rate, a move that is expected to bring relief to millions of borrowers across the country. A reduction in the repo rate generally leads to lower interest rates on loans, thereby reducing the Equated Monthly Installments (EMIs) for borrowers. This article delves into the implications of the RBI’s repo rate cut, explaining how it impacts home loans, car loans, personal loans, and business loans, while also providing a detailed breakdown of potential savings for borrowers.

Understanding Repo Rate and Its Impact

The repo rate is the interest rate at which commercial banks borrow money from the RBI. A reduction in the repo rate means that borrowing costs for banks decrease, and banks in turn often pass on this benefit to customers by lowering interest rates on loans.

When the repo rate is cut, banks reduce their Marginal Cost of Funds based Lending Rate (MCLR), which determines the interest rate on loans. As a result, loan EMIs become more affordable for borrowers.

For example, if the RBI reduces the repo rate by 50 basis points (bps), it translates to a 0.50% reduction in the interest rates on loans, making EMIs more affordable.

Impact on Different Types of Loans

1. Home Loans

Home loans are typically long-term commitments, making them highly sensitive to interest rate changes. A small reduction in the interest rate can lead to significant savings over the loan tenure.

For example, consider a borrower with a home loan of ₹50 lakh for a tenure of 20 years at an interest rate of 8.5%.

- The current EMI would be approximately ₹43,391.

- If the interest rate reduces to 8% due to the repo rate cut, the new EMI would be ₹41,822.

- This results in a monthly saving of ₹1,569 and a total saving of ₹3.76 lakh over the loan tenure.

2. Personal Loans

Personal loans typically have higher interest rates compared to home loans, and any reduction in interest rates can provide immediate relief to borrowers.

For instance, if an individual has a personal loan of ₹5 lakh for five years at an interest rate of 12%:

- The current EMI would be around ₹11,122.

- If the interest rate is reduced to 11.5%, the new EMI would be ₹10,977.

- The borrower would save approximately ₹145 per month and ₹8,700 over the loan tenure.

3. Car Loans

Car loans usually have shorter tenures compared to home loans, but even a small reduction in interest rates can lead to meaningful savings.

For a borrower with a car loan of ₹10 lakh at an interest rate of 9% for five years:

- The current EMI would be ₹20,758.

- If the interest rate drops to 8.5%, the new EMI would be ₹20,555.

- This would result in a monthly saving of ₹203 and a total saving of ₹12,180 over five years.

4. Business Loans

Business loans are crucial for entrepreneurs and companies looking to expand operations. Lower interest rates make borrowing more affordable, enabling businesses to invest in growth opportunities.

For instance, if a business takes a loan of ₹25 lakh at an interest rate of 11% for 10 years:

- The current EMI would be ₹34,485.

- If the interest rate drops to 10.5%, the new EMI would be ₹33,712.

- The borrower would save ₹773 per month and approximately ₹92,760 over the loan tenure.

How to Calculate Savings on EMI

Borrowers can calculate their potential savings using an EMI calculator. The formula for EMI is:

Where:

- P = Principal amount (loan amount)

- r = Monthly interest rate (Annual interest rate / 12 / 100)

- n = Loan tenure in months

Using this formula or online calculators, borrowers can estimate their new EMI and compare it with their current EMI to determine the savings.

Factors Influencing the Actual Savings

While a repo rate cut theoretically leads to lower EMIs, several factors influence the extent of actual savings:

- Bank’s Policy on Rate Transmission: Not all banks pass on the full benefit of a repo rate cut to borrowers. Some may delay or only partially reduce interest rates.

- Type of Interest Rate: Borrowers with floating interest rates benefit immediately from rate cuts, whereas fixed-rate loan borrowers do not.

- Loan Tenure: Longer-tenure loans, such as home loans, experience greater overall savings compared to short-term loans.

- Credit Score: Borrowers with high credit scores are more likely to receive lower interest rates from banks.

How Borrowers Can Maximize Benefits

To make the most of the repo rate cut, borrowers should consider the following strategies:

- Refinancing Existing Loans: Borrowers can negotiate with their existing lender for a lower rate or consider transferring the loan to another bank offering better terms.

- Prepaying Loans: With reduced interest rates, prepaying a portion of the loan principal can further decrease the interest burden.

- Monitoring Market Trends: Keeping track of repo rate changes and bank policies helps borrowers make informed financial decisions.

- Opting for Floating Interest Rates: Floating rates adjust with market conditions, ensuring that borrowers benefit from future rate cuts.

Conclusion

The RBI’s decision to cut the repo rate is a welcome move for borrowers, offering them potential savings on loan EMIs. Home loan borrowers, in particular, stand to gain substantial benefits over the long term. However, the extent of savings depends on various factors, including the transmission of rate cuts by banks and the type of interest rate chosen by borrowers.

To make the most of the repo rate cut, borrowers should explore refinancing options, consider prepayments, and stay informed about market trends. By taking proactive steps, they can maximize their savings and improve their financial stability in the long run.

Read more Latest News